- About

- Undergraduate

- Research

- Inclusivity

- News & Events

- People

Back to Top Nav

Back to Top Nav

Back to Top Nav

Back to Top Nav

For Economics majors interested in mathematics and finance ...

MATH 86: MATHEMATICAL FINANCE

Instructor: John W. Welborn

Email: John.W.Welborn@dartmouth.edu Office Hours: By Request

COURSE DESCRIPTION

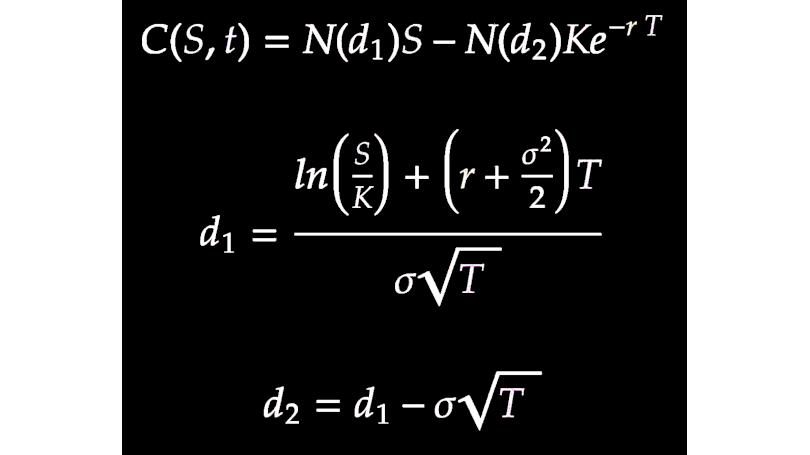

Financial derivatives can be thought of as wagers on uncertain future financial events. This course will take a mathematically rigorous approach to understanding the Black-Scholes-Merton model and its applications to pricing financial derivatives and risk management. Topics will include arbitrage-free pricing, binomial tree models, measure theory, Ito calculus, the Black- Scholes analysis, derivatives pricing, volatility modeling, and hedging.

PREREQUISITES

MATH 20 and MATH 40, or MATH 60; MATH 23; and COSC 1 or the equivalent.